Special Edition — Relaunch Issue

A Note on Our Hiatus — and What Comes Next

We owe our readers a candid explanation for the extended silence. Following our last publication, our work attracted the attention of public authorities, which introduced a layer of regulatory scrutiny that compelled us to pause operations temporarily to ensure full compliance.

That pause was not wasted. We used the period to significantly refine our investment framework, stress-testing our proprietary systems and sharpening our analytical process. We are now confident in what we have built — and we believe the timing of this relaunch could not be more relevant.

We are returning with a three-part 'big picture' series before resuming our regular cadence:

- Today: Our assessment of the Long-Term Debt Cycle

- Next Week: The Business Cycle and Mid-Term Views

- Following: Our strategy process

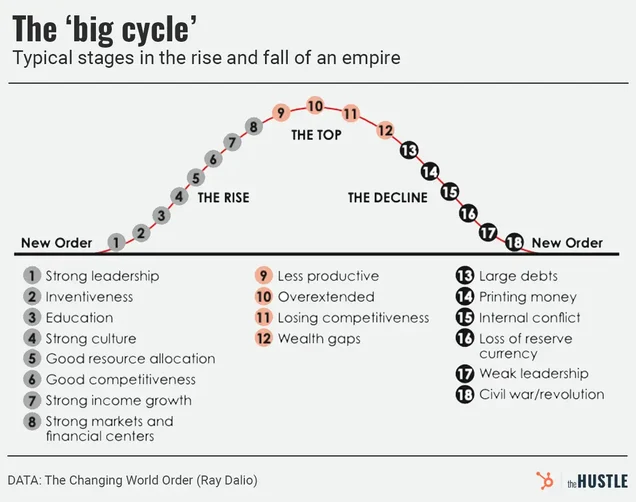

The End of the Long-Term Debt Cycle

As Ray Dalio's framework describes, we believe the global economy is currently navigating stages 16–17 of the Long-Term Debt Cycle — a juncture characterized by fiscal stress, eroding institutional credibility, and rising geopolitical competition.

Our central thesis is that markets are significantly mispricing the risk of a secular shift in the global order. We are witnessing a rare historical convergence: the external geopolitical combustibility of 1914 overlaid on the internal economic fragility of the 1930s. The future is not predetermined. However, history consistently demonstrates that when these specific conditions combine, the prevailing status quo rarely survives intact.

Part I: The Geopolitical Cycle — From Globalization to Multipolarity (Echoes of 1914)

The Illusion of Interdependence

In early 1914, the world was deeply globalized — arguably more so than today relative to GDP. Trade volumes were substantial, and the prevailing consensus held that war had become economically impossible given how intertwined national economies had become. Yet a rising Germany challenged an established Britain, and the system fractured with devastating speed.

Today, a structurally parallel dynamic is unfolding: a rising multipolar bloc (BRICS+) is challenging the unipolar hegemony the United States has held since the fall of the Soviet Union. The economic entanglements are real, but as 1914 demonstrated, interdependence alone does not guarantee stability.

The Collapse of Institutional Constraints

In 1914, governments rapidly discarded legal frameworks such as The Hague Conventions and diplomatic structures like the Concert of Europe. Today, we are witnessing an analogous erosion of the Rules-Based International Order in real time. Several developments illustrate this deterioration:

- Enforcement Failure: UN resolutions are routinely ignored by major powers without meaningful consequence.

- Selective Application of Norms: The humanitarian crisis in Gaza — backed by Western powers — alongside the EU's inability to protect member states from attacks on energy infrastructure by non-members, signals the effective end of neutrality as a governing principle.

- Executive Overreach: Unilateral foreign policy actions — in Venezuela, Iran, and Syria — have bypassed legislative oversight and violated the sovereignty principles the Western alliance once championed as foundational.

Part II: The Economic Cycle — Debt, Inequality, and Financial Repression (Echoes of the 1930s)

While our geopolitical backdrop mirrors 1914, our economic fundamentals carry a striking resemblance to the 1930s.

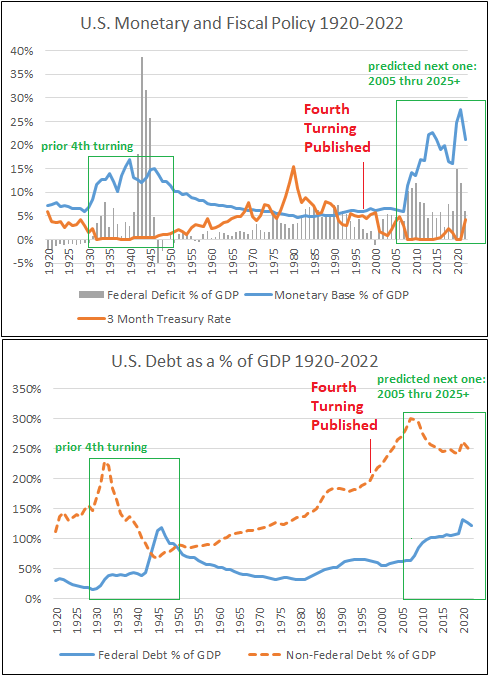

Fiscal dominance.

We have entered a period of fiscal dominance. Federal deficits are expanding structurally — not cyclically — even during periods of nominal growth. Simultaneously, the traditional buyers of Western sovereign debt have largely exited:

- Social Security has become a net seller of Treasuries.

- Japan is liquidating US holdings to defend the yen.

- China and Russia have aggressively rotated reserves into gold.

The question of who remains to absorb this supply has a clear answer: central banks. The Federal Reserve's announcement of the Reserve Management Purchases (RMP) program in December 2025 — committing to $40 billion per month in short-dated bill purchases — marks, in our view, the effective end of central bank independence. This is not liquidity management; it is deficit monetization.

Financial Repression 2.0

The mechanism of monetary stimulus has shifted from the Federal Reserve to the Treasury. We do not anticipate a return to broad open market operations or mortgage purchases. Instead, we expect the deficit to be financed through short-term issuance, with short-term rates kept artificially suppressed to make the fiscal arithmetic viable.

This is the classic playbook for sovereigns carrying debt denominated in their own currency: inflate it away slowly, over time, while maintaining the appearance of solvency.

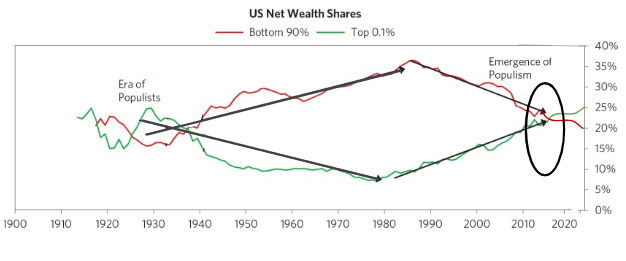

The Widening Wealth Gap

Decades of accommodative monetary policy have functioned as a structural lever for asset inflation, disproportionately benefiting holders of capital — equities, bonds, real estate — while progressively decoupling financial markets from the real economy.

Simultaneously, the labor factor has faced a sustained degradation relative to capital. Wage growth has been structurally capped by WTO-driven globalization (through labor arbitrage via offshoring) and by large-scale immigration flows that have expanded the domestic labor supply since 2022. As a result, wealth concentration has returned to levels not seen since the 1930s — a comparison that should not be taken lightly.

Political Legitimacy and the Crisis of Institutions

Institutions cannot survive when the public loses confidence in the moral standing of those who govern them. The partial release of the Epstein files was not merely a tabloid event — it served as a signal of systemic elite corruption. The implication of individuals across branches of the US government, British royalty, European leadership, and global finance reveals a pattern that goes beyond isolated scandal.

When public apologies substitute for prosecution, and when accountability appears to be applied selectively — swiftly for geopolitical adversaries but rarely for powerful domestic actors — the social contract fractures.

The Democratic Disconnect

Perhaps the most structurally concerning signal is the widening gap between policymakers and the electorates they ostensibly serve. In the United States, a clear mandate for fiscal restraint and non-interventionism has been systematically inverted. In Europe, agricultural and industrial policies are being implemented in direct defiance of mass public protest.

We view this disconnect as a late-cycle warning sign. It suggests one of two trajectories: either governments are ignoring voters because they anticipate a state of emergency in which elections become secondary to national security imperatives, or they retain sufficient confidence in their ability to manage electoral outcomes. Neither scenario is benign.

What to Expect From Here

If these factors continue to converge — and our base case is that they will — the global economy is transitioning toward what we would characterize as a War Economy structure. This does not necessarily mean widespread conventional conflict, but it does mean that capital allocation is increasingly driven by political directive rather than market efficiency.

Our Key Expectations

- Conflict and Disruption: Both internal (civil unrest driven by a fractured social contract) and external (resource competition and proxy conflicts) are likely to intensify.

- Currency Debasement: The path of least resistance for managing sovereign debt burdens is inflation. Even if central banks lower nominal rates to ease fiscal pressure, inflationary forces will remain sticky due to supply chain fragmentation and continued monetary expansion.

- War Economy Capital Allocation: In this environment, capital is increasingly directed by political priority rather than return on investment. Resource nationalization — as evidenced by recent US government stakes in strategic industries — is an early indicator of this shift.

- The Primacy of Real Assets: Tangible assets that cannot be debased or printed become the most reliable stores of value. Recent performance across commodities, real assets, and gold reflects this repricing, and we believe it is still in its early stages.

- Technological Feudalism: The US and EU are actively building the digital infrastructure for unprecedented mass surveillance and control. The rollout of Central Bank Digital Currencies (CBDCs), mandatory digital identity frameworks (including the EU's 2027 digital wallet mandate), and enhanced AML monitoring are not primarily efficiency measures. They are the instruments required to enforce capital controls and negative real rates in a high-debt, low-growth environment.

That concludes our assessment of where we stand in the long-term debt cycle. Next week, we will detail our mid-term view — the business cycle — and outline how we are positioning our portfolio within this broader context.

LINK OF THE WEEK: Luke is a great macro thinker and has been on the right side of the market for as far as I've been following him. Enjoy

Thanks for reading!

DISCLAIMER: The No Rainy-Day is not registered with any financial regulatory agencies. Content is for research, education, and entertainment purposes and should NOT be considered personalized financial advice