War scenarios: what is the market missing?

I. The Iran Conflict — The Crisis the Market Still Has Not Priced

A particular foreign policy faction in Washington has sought a direct military confrontation with Iran for the better part of three decades. They now have it, triggering a cascade across global energy markets, sovereign debt, and ultimately the financial system. The damage is real.

Whether or not that outcome was intended is a question for historians. The question for investors is simpler: what comes next, and how fast does it arrive?

The Hormuz Closure: The Largest Oil Supply Shock on Record

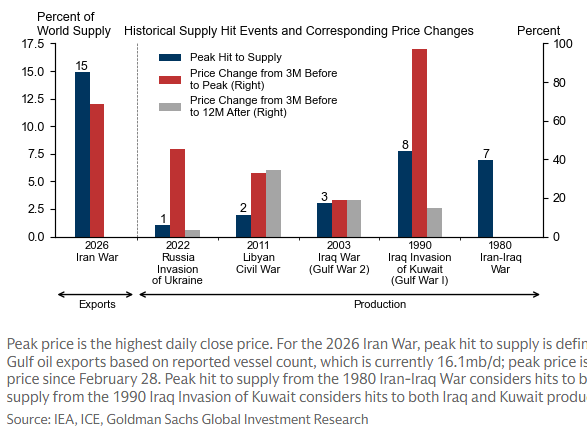

Goldman Sachs has characterised the current disruption as the largest oil supply shock on record. Not the largest in a decade, or since the Gulf War, or since the Arab oil embargo. On record. That framing should sit with you for a moment before we discuss the details.

The immediate buffer — crude already at sea, in transit, filling the gap between closure and awareness — has now been largely absorbed. What sustained the appearance of normalcy in the first two weeks is exhausted. We are now entering the phase of active rationing, emergency allocation, and government-directed supply management across most major economies. Outside the United States, this is no longer a tail risk to be managed. It is a condition to be navigated.

Hormuz is likely to remain closed for at least another three to four weeks. If that holds, the damage compounds. What begins as an energy shock migrates, through well-understood channels, into something considerably broader.

Europe’s Self-Inflicted Vulnerability

No region enters this period more exposed than Europe — and the exposure is largely self-inflicted. European leaders, with a handful of exceptions, have publicly condemned Iran while declining to acknowledge the Israeli strikes on civilian infrastructure that triggered this escalation. That may be a defensible diplomatic posture. It is not a coherent energy policy, and it is not in the interest of European citizens.

Over the past four years, Europe voluntarily severed access to cheap, reliable Russian pipeline gas in favour of dependence on US LNG spot markets. Simultaneously, it accelerated the decommissioning of nuclear generation capacity. The combined strategic logic of those two decisions was never adequately explained to the public, because there is no satisfactory explanation. The consequences are now materialising at the worst possible moment.

Current gas storage levels are materially below prior-year averages for this point in the seasonal cycle — before the conflict has fully transmitted into LNG supply chains. Europe is now competing for the same molecules as Asia, with less pricing power, smaller strategic reserves, and no viable alternative supply route. The months ahead — April through September — are precisely when European countries would normally be rebuilding storage for next winter. That process is now severely disrupted.

Why This Conflict Does Not Resolve Quickly

Markets are still pricing a relatively short-duration conflict. That assumption is, in our view, the central mispricing of the moment. Iran is not Venezuela.

Nothing measurable is de-escalating. The dominant narrative — that parties will find an off-ramp, that rational self-interest will prevail, that this is contained — is structurally identical to the narrative that convinced investors in July 1914 that war would be brief. Everyone would be home by Christmas.

We are in the escalation phase, not the de-escalation phase. The conflict is set to expand — more actors, more theatres. The US is likely to attempt a ground operation. The probability of military success is low. The probability of broader entanglement is high.

The TACO ("Trump Always Chickens Out") Problem: Why De-escalation Attempts Will Fail

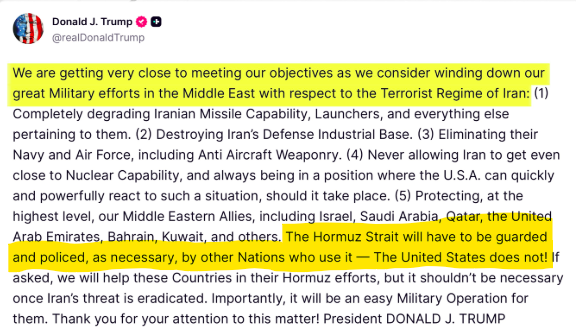

A theory circulating in political circles holds that the Trump administration is engineering an off-ramp — that the aggressive posture is negotiating theatre, and that Washington will pull back from the brink before real damage is done. The problem with that theory is mechanical. Both Iran and the bond market have a vote, and neither is providing the conditions Trump needs to declare victory.

Hormuz remains closed. Treasury yields are rising. The bond market is not providing the financial accommodation that would allow a clean political exit. Any attempt to declare success while the strait remains closed will be immediately contradicted by energy prices, inflation data, and the visible deterioration in global economic conditions.

In a significant and underreported development, the US Treasury has quietly eased oil sanctions on Iran — specifically authorising the sale of Iranian crude and refined products into the United States. Scott Bessent has described it as a “narrowly tailored, short-term authorization” for Iranian oil currently stranded at sea. Read the framing carefully. This is a de facto concession dressed in technical language to avoid the appearance of capitulation. It reveals the pressure the administration is already under.

The Second-Order Cascade: Energy to Food to Social Stability

The second-order effects are not speculative. They are on a known and predictable timeline, and the first stage is already underway.

Fertilisers, industrial chemicals, plastics, and transport inputs are all derivatives of oil and gas. They do not reprice instantaneously — there is a production and distribution lag of four to eight weeks. That lag is now expiring. Input cost inflation is beginning to hit agricultural supply chains, and it will show up in food prices four to six weeks beyond that.

The sequence is well established: energy shock → input cost inflation → lower agricultural yields and higher food prices → real income compression → social and political consequences. The final stage — when people’s ability to afford food is genuinely affected — is where energy crises historically acquire political dimensions. We are not there yet. We are, on our estimate, 10 to 12 weeks from the conditions that produce it, assuming no normalisation of supply.

The structural point is equally important: even if Hormuz reopened tomorrow, this does not resolve quickly. Supply chains that are dislocated take months to re-synchronise. Inventories that are depleted take time to rebuild. Pricing psychology that has shifted toward rationing and hoarding does not reset because a shipping lane reopens. Europe, having structured its energy policy around the assumption that global markets would always be stable and accessible, will bear the largest share of that adjustment.

This is not a temporary shock to be waited out. It is a permanent upward repricing of energy security risk — one that European policy choices have made maximally painful for European citizens.

The second-order effects are not speculative. They are on a known and predictable timeline, and the first stage is already underway.

II. The AI Productivity Trap — A Credit Problem in Formation

The Iran conflict is the acute crisis. What follows is a slower-moving structural failure that has been building for eighteen months — and is about to collide with the credit cycle at the worst possible moment.

Goldman Sachs has published the most consequential and least-discussed economic finding of the quarter: after $450 billion in AI capital expenditure last year, tens of thousands of layoffs executed in the name of AI-driven restructuring, and the wholesale replacement of entire departments with automated systems, artificial intelligence contributed essentially zero to measured economic growth.

This is not an argument against AI as a technology. It is a data point about the gap between narrative and measurable output — and, more importantly, about where the capital actually went.

The $450 billion did not flow into productivity improvements that raised wages, reduced prices, or expanded economic output. It flowed upward — from the payroll budgets of eliminated workers directly to Nvidia’s revenue line. $130 billion in GPU sales, record net margins, and share buybacks. The money moved from labour to capital, and then from capital to a handful of semiconductor companies. The economic multiplier of that transaction, for the broader economy, is close to zero.

The companies that executed these restructurings — Atlassian cutting 1,600 roles, Meta eliminating 21,000, Block cutting 40% of its workforce, Amazon reducing warehouse headcount — bear the fixed costs of having dismantled their human operating infrastructure. The variable costs they eliminated (salaries) are gone. The revenue they expected AI to generate or preserve has not materialised at forecast rates. The business model assumed automated systems would produce at least as much economic value as the people they replaced. For most companies, that assumption has not been validated by the data.

The jobs are already gone. The growth did not come. The productivity did not come. The revenue did not come. What came instead was a $130 billion transfer to Nvidia’s shareholders.

From Earnings Issues to Credit Event

This would be troubling but contained if it were merely an earnings story. It is not. It is a credit story — and the transmission mechanism is the one that nobody is mapping.

- Between $40 billion and $150 billion in leveraged corporate loans were extended to companies whose revenue models assumed sustained human employment at scale.

- The debt service capacity of those companies is therefore lower than the models used at origination assumed.

- Those loans are packaged into CLOs. Deteriorating loan performance cascades into CLO tranche impairment.

- The pension funds and institutional investors holding those CLO tranches absorb the losses — meaning the end holder is, in many cases, the retirement savings of the workers who were eliminated in the first place.

In 2008, the financial system extended credit against residential real estate, assuming national house prices would not fall. The assumption failed. In 2026, the financial system extended credit to software companies against a promise of future cash flows. AI has invalidated that assumption faster than anyone underwrote for. The defaults have not yet arrived, but the conditions for them have been established.

The collision with the current macro environment is what makes this particularly dangerous. Companies are entering a period of rising input costs from energy, slowing consumer demand from real income compression, and tightening credit conditions from bond market volatility — all while carrying the dual burden of unrealised AI capital expenditure and reduced productive capacity from workforce reductions. Credit stress is not arriving from one direction. It is converging from three simultaneously.

Connecting the Dots

A geopolitical shock of potentially historic scale is underway in the Middle East. It is transmitting into energy prices, which are transmitting into inflation expectations, which are transmitting into bond volatility, which is tightening collateral conditions across the entire financial system. That systemic tightening is arriving simultaneously with a structural credit problem embedded in the AI investment cycle — a problem the market has not yet recognised, built on a simple and falsified assumption: that AI capex would produce proportionate economic output. It did not. The debt that funded it remains.

Equity markets are in the early stages of repricing both risks at once, with liquidity draining at twice the prior decade’s extreme and a historically unbroken bear market signal now active. Against that backdrop, gold is correcting in a global liquidity event that mirrors every major prior crisis — while institutional investors use the selloff to build the largest options position in recorded gold market history, at strikes that imply not a bear market but a monetary event. Bitcoin is rallying because a state-linked seller was accidentally eliminated. The bond market is flashing the highest volatility readings since the conflict began.

DISCLAIMER: No Rainy-Day is not registered with any financial regulatory agency. All content is provided for research, educational, and informational purposes only and does not constitute personalised financial advice.